General insurance market update

As your dedicated insurance representative, we’re constantly monitoring the insurance market to better understand and assess insurance trends and how they may affect your business.

Firstly, having the correct sums insured for the current replacement value of your building, contents and machinery, is crucial. The recent impacts of inflation, labour shortages, persistent lower AU$ (around 0.70 cents to US$ as at April 2023) and supply chain issues have caused a dramatic increase in the costs to rebuild/repair properties and replace items. It’s important that we work together to ensure you have the correct valuations and sums insured for your insurance policies.

As your adviser, we recommend that property and other asset values be reviewed regularly to ensure you’re adequately insured. Having incorrect insured values could result in any claim being adjusted due to underinsurance, meaning you could receive substantially less in a claims settlement than what you need to replace your property. Having a professional valuation will help to prevent this and we can arrange access to experienced quantity surveyors who can accurately confirm building rebuild costs for commercial and domestic buildings, in addition to plant and machinery.

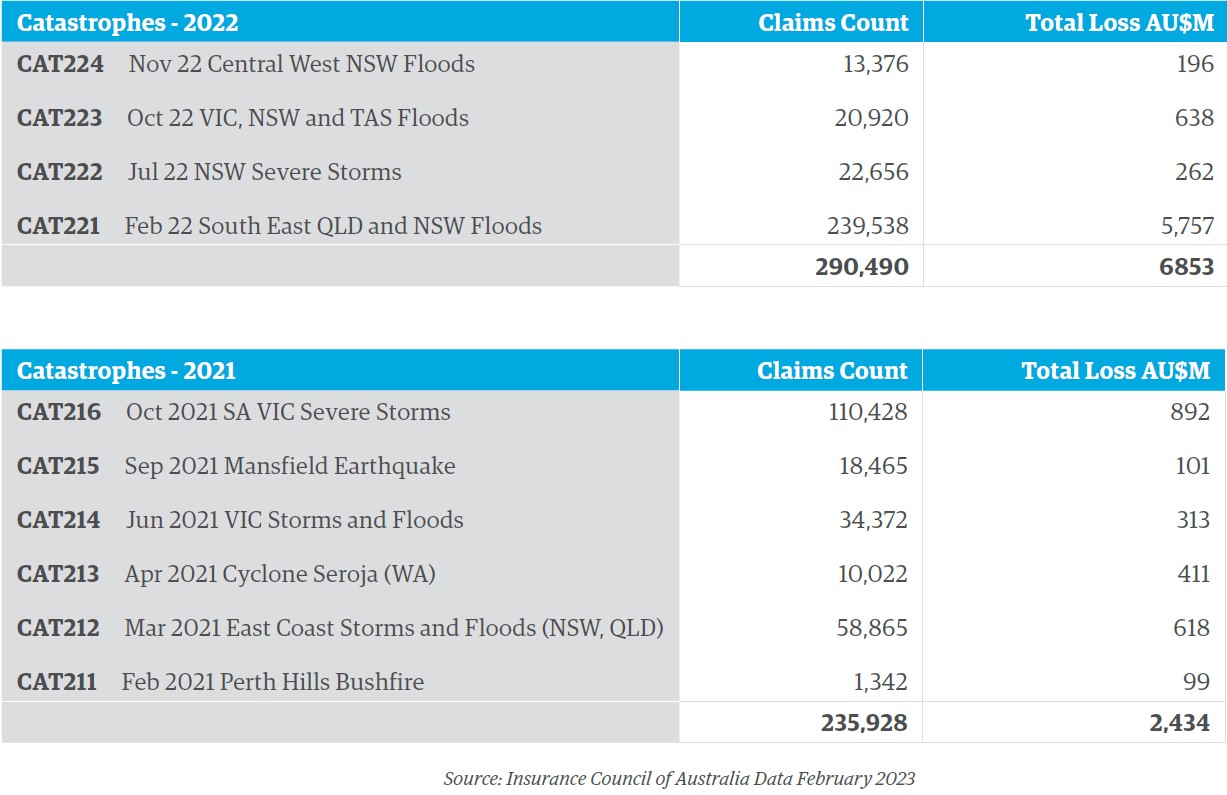

Over the last two years, Australia has had an extremely high frequency of catastrophe events, as shown in the tables below. The South East Queensland and New South Wales Flooding event is now Australia’s costliest Insurance Catastrophe. This event has had over 239,000 claims at a current estimate of AU$ 5.7B.

Pricing Outlook

In summary, the following are the key “positives” and “negatives” that will impact insurance premiums in the foreseeable future over the next 12-18 months.

Positives:

- Continued improved profitability of Insurers on the back of higher premium prices

- Bureau of Meteorology is now predicting a weakening of La Niña conditions, which is predicted to see a reduction of the high rainfall events

Negatives:

- Extreme weather events still likely

- Substantially increased reinsurance costs for Insurers are predicted in the June renewal season, due to the significant weather-related claims that occurred in 2022

- Continuing inflation impacting sums insureds, rebuilding costs coupled with persistent lower AU$

One of the key drivers for Insurers’ improved profitability in 2022 was the release of significant claims reserves provisioned for Business Interruption claims that were lodged as a result of the impact COVID had on many businesses. The High Court decision handed down in October 2022 favoured Insurers and hence they could release claims reserves that had been held pending the outcome of this High Court decision.

Given the large number of weather-related claims paid and increased reinsurance costs, pricing increases will continue on the same trajectory as we have seen over the last few years. The continued hard market will see average increases in the vicinity of 9% – 12% for Commercial Insurance, 15%+ for Property risks, including Home, and a Motor increase of 7%+, with some potential easing of Liability/Professional line classes due to the longer-term improved outlook for investment returns on reserves held for liability classes of insurance, particularly if inflation does reduce, lowering the impact of claims inflation on claims reserves held by Insurers.

With the continuing hard market, we anticipate:

✓ Continued period of higher or increasing premiums

✓ Getting insurance coverage could remain a challenge and get harder to negotiate terms

✓ Insurers still reducing capacity with some risks or industry groups or clients with prior claims

✓ Higher excesses

✓ Focus on risk management and mitigation processes

✓ More time and additional information required to place or renew insurance.

Looking to the future

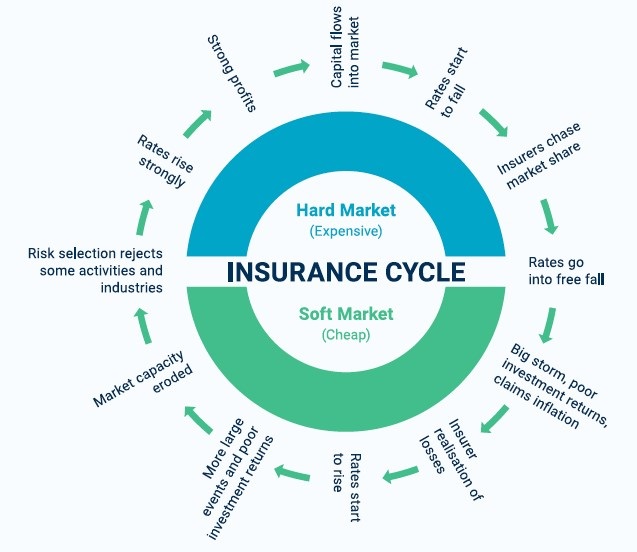

We believe the insurance industry remains at 10 o’clock on the Insurance Clock. How long it remains there largely depends on the frequency and severity of future catastrophic weather events and inflation (impacting claims repair costs). We believe average premium increases will remain in the range of 9%-15% with the exact figures being influenced by industry sector, geographic location, prior claims experience and approach to risk management.

Structural change and cost cycles are part of every industry and the Insurance Clock is a useful tool in identifying where Insurance rates are now and where they’re likely to be heading in the future.

Should you have any questions or would like to arrange a valuation or discuss any other general insurance needs, please don’t hesitate to get in touch. We’ll be very happy to help.

![]()

![]()